How to Accomplish a Techxit: Part 2

By AJ Ayers, CFP, EA

This is Part 2 of 2 of our Techxit series. In the last post (which you should most definitely read), we covered the Techxit basics and the first step of exercising your equity.

The Techxit (like Brexit). In other words: work at a high-paying tech job earning a high salary with a generous equity package and then quit after a few years, once that equity has vested and there’s a liquidity event (your company is acquired or goes public). Then the plan is usually to use the incredibly valuable skills learned in the fast-paced, high-growth environment for good: to help an environmentally conscious start-up or a non-profit who could really use those skills but can’t afford to pay competitive salaries to lure talent away from the Googles or Facebooks of the world.

Caveats, disclaimers, and general warnings: First of all, this is not tax or investment advice. This is a case study presented for your entertainment and perhaps to spark your curiosity. Second of all, this strategy is neat but the stars have to align for this to work. Third of all, this strategy goes against what I often recommend to my clients which is to diversify out of a concentrated position as fast as possible in the most tax-efficient way. This isn’t a science, it’s an art: balancing the risk of holding shares longer with the tax consequences of selling sooner.

Finally, if you have equity compensation, especially Incentive Stock Options (ISOs), you MUST go to an accountant that is familiar with this space. As you’ll see later, ISOs generate a multi-year complicated tax wormhole and my colleagues and I have found and corrected DOZENS of mistakes by other accountants. It doesn’t make them bad accountants, it just means they don’t specialize in this niche. If you want to know if your financial adviser or tax adviser knows their stuff ask them about form 3921 - that’s the tax form that reports your ISO exercises to the IRS.

Let’s pick up where we left off…

Step 2: Wait for a liquidity event.

Now that you hold these shares you’ll need to wait at least 365 days before you can sell them but to pull off a Techxit, you’re going to hold these shares for a while - probably years. Your shares will likely be transferred to a brokerage firm like E*Trade or Morgan Stanley in the meantime where you will continue to hold them. Let’s keep running with Example 2 and say that the IPO happens in April of 2016 at a price of $50.

Step 3: Stick around for another year or so and immediately sell any new equity awards as they vest. Bonus: move to a state with no income tax like Washington, Texas, or Florida.

ISOs can make you rich if the stars align, but the slow and steady way to build wealth is by saving a high percentage of your income. When companies do well, they reward employees with equity grants. When the company goes public, there are lots more shares to play with so often employees are granted additional equity - usually in the form of Restricted Stock Units (RSUs) or Non Qualified Stock Options (NQOs). I want you to think of these types of equity as income. With RSUs, the company grants you shares, there’s no special ISO/AMT treatment, it’s just plain old compensation that happens to be in the form of shares instead of dollars and is taxed accordingly. For NQOs, you still have the OPTION to exercise, but when you do, that bargain element is taxable income that will show up on your paycheck.

We’re trying to accomplish a Techxit here so we need to move out of a concentrated position. You’ll sell RSUs as soon as they vest for cash and invest the proceeds in a diversified portfolio where you own thousands of stocks and bonds instead of just one. With the NQOs, you’ll do a net exercise to generate cash as well. There’s no sense in holding these shares unless you’re in it for the long haul (which you are not, you’re getting out). Let’s make some large assumptions to illustrate my point.

If you move to a state with no income tax you could save 10% or more on income tax. Seriously, I tell my clients to move to Seattle or Austin all the time. One family even listened! In this example, moving from Brooklyn to Austin could save you $55,000 in state income taxes. Some states like California have “clawback” rules that won’t let you escape the state taxes even if you move out of the state, so watch out for those.

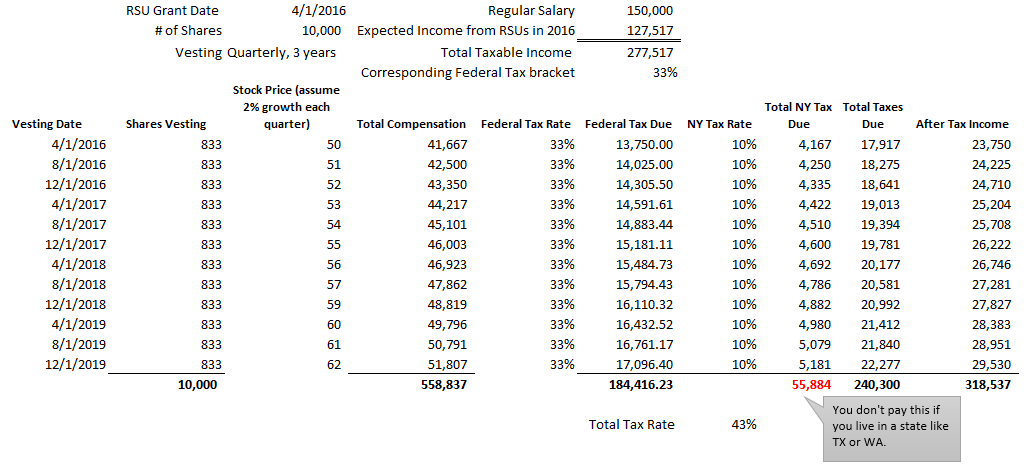

Here’s a typical RSU vesting schedule and the corresponding tax result. You cannot control the timing of RSUs. There’s nothing to exercise, you just GET the shares when the vesting date arrives. We generally recommend selling these shares and converting them to cash to invest elsewhere as soon as they vest since you’ve already paid tax on them (remember, think of RSUs as ordinary income).

So in this scenario, we’ve generated $318,537 dollars that can go straight into buying freedom.

Step 5: Start earning that AMT credit back.

So the great thing about AMT is that you can actually retrieve most of that tax you paid. The AMT that you pay in the year you exercise ISOs sucks, but in future years where you don’t exercise ISOs, your REGULAR tax will actually be higher than the estimated AMT tax. The credit works in reverse: when your regular tax due is higher than the tentative tax due (it is for MOST normal people who don’t exercise ISOs), you start to get some of that credit back. In our example in 2015, there was an AMT bill generated of $20,050 from an ISO exercise. That was the only year of exercise so you can see that in the following years the regular tax is lower than the tentative minimum tax so they will slowly earn some of that credit back ($8,398 back in 2016, $7,649 back in 2017 and so on). Here we can see that it takes 3 whole tax years to get all of the original $20,050 credit back.

Step 5: Quit your job, earn very little income for the next year and move to a state with no capital gains tax to sell your stock at 0%-15% capital gains.

You’re still holding those shares. You bought them for $1 each, which means that’s your “basis.” Because you’ve held them for more than 365 days, when you sell the shares you’ll be subject to capital gains rates, NOT ordinary income rates.

Take a year off from Roth conversions as well. You really don’t want to generate income tax here.

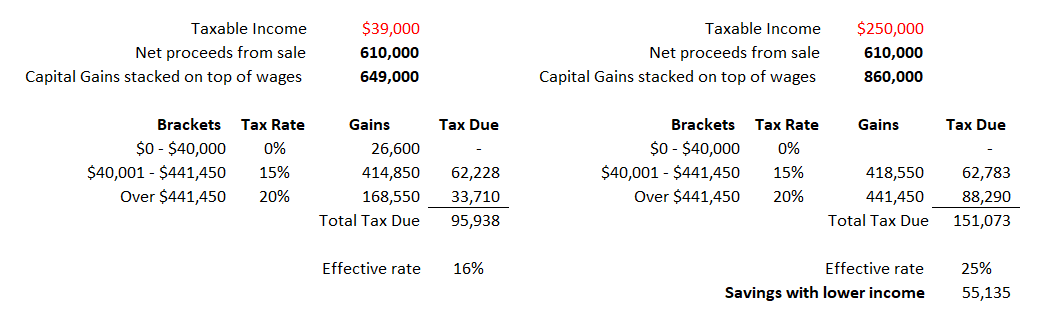

Here are the capital gains rates.

I’m sorry, wait. Did you say 0%? So you’re saying that if I sell my shares that I paid $1 for back in 2015 for their price today, I can pay 0% in capital gains? That’s right! To an extent. You’ll fill up the 0% bracket pretty fast and most of your gains will be taxed at 15%. Major caveats here: you aren’t going to actually pay 0%, you’ll pay the Medicare investment income tax of 3.8%, and potentially some additional capital gains taxes.

Now, like income tax brackets, the long-term capital gains brackets are blended. Meaning your gains could potentially be taxed at 0%, 15%, and 20%. How the ordinary income and capital gains rates blend together is complicated and beyond the scope of this rant so this grossly oversimplified example is shown to illustrate the blended rates.

Personally, I’d much rather pay 15% in long term capital gains than 20%, HOWEVER, the longer we wait to sell out of this concentrated position, the more RISK we’re taking. The risk is this: we’re excited about exiting at a price of $62 but then a competitor gains market share and now our shares are worth half of what they were at $31. Remember, you can’t control the future.

So let’s review this extremely oversimplified and convenient example that hopefully shows you how this shit works.

Step 6: Invest your proceeds in a diversified portfolio and take advantage of compound interest.

You did it! You could take your $847,000 and buy a modest home in cash (usually a bad idea) or have a sizable downpayment on your dream home. But the real move here is to invest the proceeds into a diversified portfolio. Historically the US stock market has returned on average 8-10% per year (experts argue, we use 8% in our projections) but in this example, let’s be conservative and say we can earn 5% on our money. If you invest that entire nest egg in a portfolio that grows on average 5% a year, you’ll have 1.36 million dollars in ten years.

Go forth and Techxit my friends!

Things that Can Wreck Your Techxit

1. Love

You fall in love and get married to a badass high-income earner. I mean I HATE it when this happens to my single clients (note the sarcasm here). You could spend years planning and executing a Techxit only to fall in love with a Senior Vice President who makes $400,000 annually. If you get married, that 0%-15% capital gains rate is a lot harder to achieve with two people.

How to fix it: Convince your new spouse to quit their job as well and travel the world with you while you sell off the remainder of your equity.

2. Volatility

Not only will the stock price be bouncing around with the potential to fall dramatically and never recover (like Blue Apron) but you will have to ride the emotional wave of when to sell. You are going to feel like the smartest person in the world if you sell at a 52-week high and/or the dumbest person in the world if you sell at the 52-week low. If your company is a stinker and the stock price never goes much above your exercise price, your Techxit could be a failure.

How to fix it: You can combat your own emotional reactions to the stock price by acting like a CEO with insider information. Most CEOs and other high-ranking executives have their stock sales and purchases strictly regulated by the SEC because these folks are directly in charge of the growth of the company. These folks are often required to disclose their planned sales well in advance of making important decisions about the company. In fact, they have to sign a document that lists out every share sale for a certain period, this is called a 10b51 plan. I have some of my clients create a mock 10b51 plan so we have a plan and stick to it.

3. Golden Handcuffs

“Just ONE more year until my next crop of shares vest,” is what you might tell yourself. Or, “I can’t walk away from $200,000 of unvested RSUs, I’m not necessarily unhappy in my current role.” There’s a reason equity compensation exists and it’s not because your employer loves you. It’s usually because your work generates revenue for your employer and they want to keep you around. It doesn’t have to be money, but it could be a new part of the business you’ll head up or an impressive title change that keeps you there. Your employer is probably going to try and pull a few tricks to get you to stay: how does another $100,000 in NQOs sound?

How to fix it: Stick to the plan but it’s still okay if you want to change your mind and stay.

4. Dream Job Part II

Imagine this: you’re sitting at a table in a cafe in Casablanca having an espresso, you’re three months into your worldwide tour of the famous places that appear in your favorite films. You check your email and there’s this insane offer from an old friend to be the #2 at an exciting start-up. You think, “But wait, this was supposed to be my year off.” This is an offer you really can’t refuse so you decide to haul it back to the states and become the CTO of what promises to be the next Etsy. There goes your no/low-income year. Ohh well, you’ll probably still only pay 15% on those long term capital gains.

How to fix it: What are you nuts? Don’t let taxes get in the way of living your life!