Renting vs Buying Your Home: The Ultimate Showdown

This is the 4th iteration of this popular webinar, and was hosted by AJ Ayers and John Owens, of Brooklyn Fi. They took on the age-old question: Is it better to rent or buy a home? These are the takeaways, as well as some resources to help you in your decision-making process.

Key Timestamps:

NYC: A Real Estate Rollercoaster of a Case Study (03:45)

The Interest Rate Saga (06:07)

Team Rent: John's Top 10 Reasons (11:45)

Team Buy: AJ's Top 10 Reasons (20:35)

Q&A (35:10)

Setting the Stage:

Basic Facts and Assumptions

Home values increase about 3% per year on average

Average rents increase about 2% per year (except in NYC recently)

Average homeownership duration is 7 years

Assumed 8% annual return on stock market investments

The New York City Real Estate Rollercoaster

Manhattan studio apartments: 8% annual rent increase

Average Manhattan studio rent: $3,604

Median Manhattan rent across all types: $4,667

Brooklyn also seeing 8% year-over-year rent increases

Unprecedented rent increases pushing some towards buying

Advice: If you have a good deal on rent, consider locking it in

NYC traditionally a great city for renters, but dynamics are shifting

Current NYC market described as a "shit show" for renters

The Interest Rate Saga

Recent rate cut by Federal Reserve: 0.5%

Historical perspective on interest rates

Potential impact on housing prices and affordability

Current rates still higher than what many are used to

Housing supply issues stemming from 2008 financial crisis

Mismatch between economic textbook theories and current market reality

Possibility of housing prices increasing as rates decrease

Advice to consider buying now if you're definitely in the market

Importance of understanding true affordability, not just what banks will lend

Medium sale price for homes in July 2024: $430,000 (near all-time high)

Housing supply remains tight, affecting market dynamics

New York Rental Prices: A Zillow Deep Dive

Zillow offers comprehensive data on rental prices and market trends

Includes median rent, monthly and yearly changes, and rental unit numbers

Useful for landlord negotiations and market understanding

Manhattan median rents around $4,000, studios averaging $3,600

Brooklyn also seeing significant price increases

Overall NYC rental market described as "expensive"

Team Rent:

John's Top 10 Reasons

10. Browsing Zillow is a hobby, not an investment

Housing is ultimately a cost, not an investment

Don't get caught up in keeping up with friends

Not every home on Zillow is a good investment

9. Buying a home is more complex than you think

Requires a team: attorney, broker, inspector, mortgage lender, financial advisor

Emotional rollercoaster during the buying process

Especially challenging in popular markets

8. Low transaction costs for renting

No 20% down payment required

No real estate commissions or closing costs

Fewer surprises and unexpected expenses

7. Property Taxes & More Issues When You Buy

You can always move if your rent goes up, but you’re stuck with your mortgage

HOA fees can get to $1,000 or more per bedroom

Home assessments can equate to not-so-fun surprise fees.

6. Diversification advantages

Buying concentrates wealth in one asset

Homes are not liquid assets

Renting allows for more investment opportunities, like for your business.

5. Homes aren’t always great investments

Often a huge time and money sink

Success stories often omit costly details (hundreds of thousands spent on repairs/renos)

Price appreciation typically not huge, and it’s an illiquid investment

4. Nobody keeps their house the way it is

When you feel the NEED to renovate, you’ll probably go over budget

Many people forget to consider these expenses in their analysis

3. Selling your home can be hard and expensive

Can take a long time to sell

Potential for unexpected obstacles and expenses (e.g., liens and renovations)

Strain on life plans and relationships (Leaving the house for 23423 showings)

2. Cash flow considerations

Owning has many extra costs beyond mortgage

Rent is your ceiling, mortgage is your floor for housing costs

Easier to adjust housing costs when renting

1. Flexibility for life changes

Quitting job, relationship changes, moving cities

Renting allows for quicker, easier transitions

Selling a home can complicate major life changes

Team Buy:

AJ's Top 10 Reasons

10. Access to cheap or gifted capital

Banks more likely to loan for homes than other investments

Family members more willing to gift money for home purchases

Opportunity to leverage significant amounts of capital

9. Mortgages are awesome

Mortgage interest deduction

Property tax deduction (with some limitations)

Up to $250,000 tax-free gain per spouse when selling primary residence

Quick Lesson: How Mortgages Work (slides 32-34, all are charts)

Early years: Payments mostly go towards interest

Mortgage interest often tax-deductible (up to $750,000 loan)

Interest portion decreases over time

Rates significantly impact total interest paid

Example: 3% vs 6.75% rate difference = $30,000 more interest annually

Advice: "Marry the price, date the rate"

Refinancing possible if rates decrease

Higher rates dramatically affect monthly payments

Example: $2,000 difference in monthly payment between 3% and 6.75% rates

8. Automated savings mechanism

Good for people who struggle with saving

Less likely to skip payments due to consequences

7. The Market: potential to pick a winner

Opportunity to find great neighborhoods or get deals

Possibility of significant appreciation in certain markets

Example: Buying in Austin, Texas in 2009 (sell for a huge profit or avoid the 30% yearly rent increase)

6. Taxes!

A lovely mortgage deduction

Property tax deduction (limited under the Tax Cuts and Jobs Act of 2017)

5. Security and stability

Having a place of your own

No landlord to potentially evict you

Ability to have as many pets as you want

Stability for children and elders

4. Tangible and easy to understand

Real estate is more concrete than the stock market

Easier for family and friends to appreciate- throw a housewarming party!

The stock market can be intimidating

3. Building equity over time

Paying down mortgage principal

Potential for home value appreciation

Opportunity for "flipping" in rapidly appreciating markets

2. Lock in a low housing payment

Fixed mortgage payments (if not refinancing)

Protection against rising rents

Could retire without mortgage or rent costs because you own your home

1. The "feels good" factor

Sense of accomplishment and stability

Creating a home that truly feels like your own

Opportunity for custom improvements (e.g., bookshelves!)

No clear winner between renting and buying

Decision depends on individual circumstances and goals

Key factors: financial situation, life stage, career plans, lifestyle

Renting favors flexibility and transitional phases

Buying suits stability-seekers and those ready for commitment

Make an informed decision based on your unique situation

Remember: The winning choice should fit your life and long-term objectives!

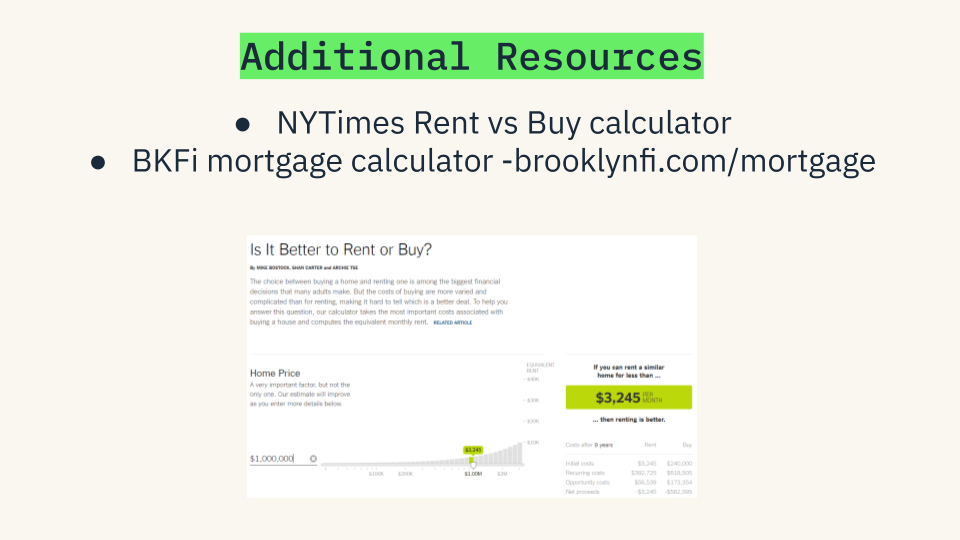

Additional Resources for Your Housing Decision

New York Times Rent vs. Buy Calculator

Helpful tool for evaluating the rent vs. buy decision in detail

Allows users to input various factors and compare scenarios

Features a mortgage calculator

Whether you're Team Rent or Team Buy, this decision's as personal as your coffee order (and pricier).

But don't sweat it! BKFI’s team can help you figure out the right timing and align your eventual decision with your financial goals.

Have questions about your specific situation?

We’ve got your back. Talk to a Brooklyn Fi advisor today — no house-hunting squats required!