What We Can Control: A Reflection on Tariffs, Market Volatility & Action Steps We Can Take Right Now

by John Owens, CFP®, EA, ECA, CPWA®

When the world feels shaky, it helps to focus on what’s steady.

Recent headlines have been unnerving (to say the least), and markets have reminded us how little control we have over short-term movements. But that doesn’t mean we’re powerless. These are the moments when it matters most to ground ourselves in the basics: what we know, what we’ve planned for, and what we can do today.

This past week, I went back to my own fundamentals - not just as an advisor but also as an investor, a business owner, and a person with real obligations and goals. I thought it might be helpful to share how I’ve been approaching this stretch of volatility, both practically and emotionally.

I can’t control the markets (sadly). Nor the tariffs. I can’t control that certain asset classes are getting hit harder than others.

Focus on What You Can Control

You Can Control

- ➤ Your savings rate

- ➤ Your living expense

- ➤ Diversifying your portfolio across thousands of companies

- ➤ Your ability to defer taxes (saving in your 401(k)/IRA)

- ➤ Expense Ratios

- ➤ Your emotional reaction to those things over there ⟶

Significant impact on Long-term Wealth Building

You Can't Control

- ➤ Tariffs, a global pandemic or other crisis

- ➤ Political climate

- ➤ The latest Reddit /personalfinance and /wallstreetbets trends

- ➤ Volatility of the stock market

- ➤ Your friend Phil who won't shut up about the $100,000 he just made trading stocks

- ➤ Tax rates

Small/medium impact on Long-term Wealth Building

Step #1: I stopped looking at my portfolio’s rate of return

The first thing I did was stop looking at my own portfolio’s rate of return. While I have access to the same tools our clients use and invest my money the same way we manage portfolios for clients, I don’t need to check daily to see how much I’m down right now. I’m not planning to use the vast majority of my savings for a very long time.

Today’s value and price is no more or less important than the value and price of ANY other day that I’m not planning to use all the money. Hell, even if I was retired and living off this portfolio, today’s value and price matters little in the course of a 30-year retirement, so why focus on it?

Step #2: I double-checked my emergency fund.

The next thing I did was double-check my emergency fund. Those of you who know me well know that I like a bigger emergency fund than most. As a single guy, one-income household, and a business owner as a partner here at BKFi, my situation is a bit riskier than others - keeping in mind that our revenue has a decent correlation with the market.

Savings Order of Operations

Generally speaking, to reach financial independence, we recommend at least a 20% savings rate.

Cash

Keep roughly 1 month of living expense in checking.

Establish emergency fund (3–12 months living expense).

Tax Advantage Investing

Max out 401(k) – up to $23,500 per year

Fund a 529 Plan to Pay for College

Consider funding an IRA or Roth IRA

Investing

Fund a taxable investment account to fund financial independence.

Fund a Donor Advised Fund for charitable contributions.

Looking at my budget year-to-date, I confirmed that I have approximately 18 months of expenses in cash currently. More than enough to keep the lights on should things get hectic. Now would be a good time to restock that emergency fund cushion if you don’t have 3-6 months in cash currently.

Step #3: I noted any extra cash & reviewed my financial plan.

After validating that my emergency fund was in good shape and that I had cash set aside for any other big expenses in the next few months, I started to run some numbers for extra cash. 18 months for an emergency fund, plus cash for a trip or two this summer, seemed a bit excessive.

Next, I reviewed my Right Capital financial plan. Yes, I have one of those too. I nerd out on scenarios of my own from time to time, but primarily use them to ensure I’m on track. Like many of our clients, while the market moves shifted my investment balances down a bit, the probability of success in my plan barely flinched.

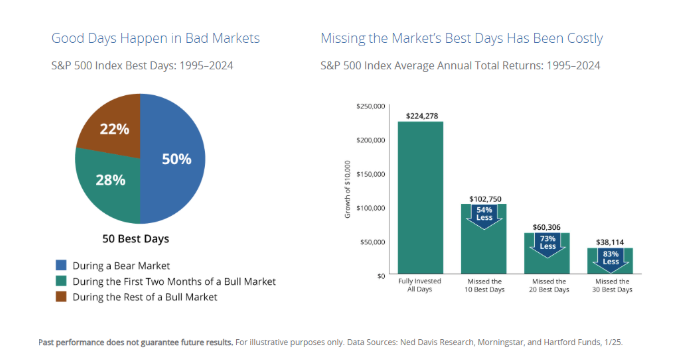

The fact is that when markets go down, expected future returns typically go up - having less money now and staying invested typically translates to making more money in the future.

So with that in mind, on Thursday last week, I took about 1.5 months of that extra cash and put it in the market. Buying into the sell-off.

And then I woke up Friday, saw the market sell-off again.

Now in hindsight, had I been a little slower to the draw on checking my cash flow, I could have made my purchase a day later and at a little lower price. And I’d be lying if I said that didn’t cross my mind. But then again, if I was able to see the future, I really wouldn’t need an emergency fund at all.

So Friday I promised myself that I’d look at the numbers again a little bit this weekend, and see if I wanted to buy more this coming week as the market sold off.

Volatile times like this make us all want to do something—to take some sort of action when elements of this feel so far out of our control. What we do (or don’t do) in times like this will have a significant impact on our long-term financial well-being.

Actions We Can Take Right Now

If you’re looking for some action to take, here’s a few to consider:

1. Upset about tariffs, trade policy, or the President’s moves - call your legislators. Let them know. It’s unclear it will help, but it certainly won’t hurt.

How to call your congressman: https://www.house.gov/representatives/find-your-representative

2. Gut check that emergency fund number. Not sure if it’s still accurate? Our team can help with that.

3. If you have some extra cash, consider putting some of it in the market. If anything else you routinely buy at the grocery store went on sale, you’d likely purchase more of it, not less. The chart below shows how despite having positive returns 34 of the past 45 years, the S&P 500 still had an average pullback of 14% annually. Buying when the market has sold off over 13% is rarely a bad move in the long-run; but may take time to pay out.

4. Recommit yourself to long-term investing. Take a step back and assess the actual timeline for the funds in your portfolio. It’ll seem rather vast compared to just a few days.

5. Grab some time with our team to review your Right Capital plan and ensure it’s on track.

Catch up on other planning items well within your control that got pushed to the backburner - like updating your estate plan, filling out that life insurance application, or opening that 529 for a new family member.

In a time of such uncertainty, we must refocus on what we can control, do a vitals check on our financial situation today, and recommit ourselves to being long-term investors as the best course of action. We must also let ourselves feel the range of emotions that come with volatility and uncertainty.

We know this kind of market environment can be unsettling. But your financial plan is built for times like these. We’re monitoring portfolios carefully, and our investment process remains disciplined and focused on the long term.

If you’re feeling uneasy, that’s normal. But you don’t have to go through it alone. We are here, we are watching closely, and we are committed to helping you stay on track, no matter what the headlines bring.